Thanks!

If you liked this, we would love for you to share it with more people.

.png)

Imagine checking your fintech platform one morning, only to realize a large transfer went to an account that doesn’t even exist. By then, the funds are gone, moved across multiple accounts in minutes, leaving you scrambling to contain the damage.

Welcome to the reality of modern fintech fraud.

In fact, fraud in fintech has moved far beyond stolen cards and basic phishing. Criminals now leverage AI-generated voices, deepfake executives, and synthetic identities to trick systems and people alike. From unauthorized account takeovers to crypto scams, fraud is becoming faster, smarter, and harder to catch. And if you’re not paying attention, it can hit your business before you even know it.

In the past, fintech fraud detection systems worked like a safety net after the fact: transactions were processed first, then reviewed. If something looked suspicious, your team could step in before the money was gone.

However, with instant payments today, that safety net is gone. Money moves immediately, so any missed warning signs mean losses happen in real time.

The problem gets worse when different parts of your system, like onboarding, login checks, and transaction monitoring, operate without shared signals. For example, information gathered when a customer signs up might not influence how their login is monitored, and unusual logins might not affect whether transactions are approved. Each step is evaluated separately, without a full picture.

Without shared context, warning signs are missed, and in fast-settlement systems, missed signals translate directly into loss.

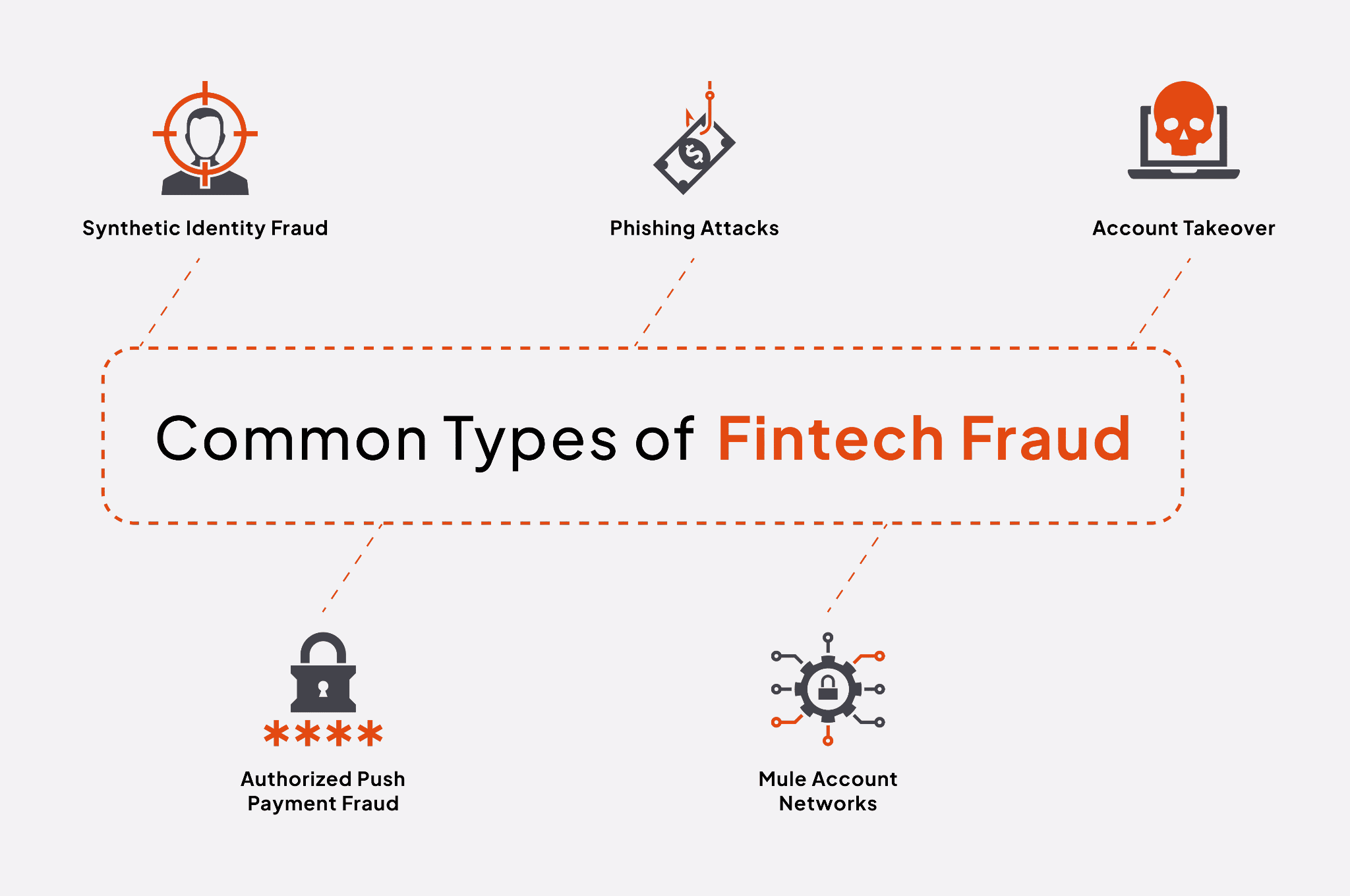

Several common fintech fraud schemes reveal where systems break down.

Synthetic identity fraud combines real and fabricated information to create accounts that pass document checks but do not correspond to actual individuals. In many segments, synthetic identities represent a significant share of new-account fraud, exposing the limits of document-only verification.

More broadly, fraudsters also create fake accounts using fabricated or manipulated identity details during onboarding. When identity checks rely on limited verification signals, these accounts can remain active long enough to be used for payment fraud or mule activity.

Phishing attacks are another common entry point. Fraudsters use deceptive emails, messages, or cloned websites to trick users into revealing login credentials. Once those credentials are captured, attackers can access legitimate accounts.

As a result, account takeover occurs when stolen credentials are used to access legitimate accounts. If authentication is treated as a one-time event, suspicious behavior during active sessions can go undetected.

Meanwhile, authorized push payment fraud relies on manipulation rather than system intrusion. Because the customer initiates the transfer, systems that rely solely on user authorization may overlook unusual beneficiary changes, sudden increases in transfer amounts, or abnormal transaction timing.

In addition, mule account networks distribute funds across multiple accounts to avoid detection thresholds. Individual transactions may appear normal, but links emerge when devices, beneficiaries, and transaction paths are analyzed together.

Taken together, these patterns point to the same weakness: systems that evaluate risk in isolation leave gaps between stages.

To address these gaps, fraud prevention must combine several complementary controls that work together across the customer lifecycle.

Risk evaluation should combine device data, behavioral patterns, transaction history, and recent account activity into a scoring system that updates continuously. As risk indicators increase, additional verification can be applied. Conversely, when behavior remains consistent, transactions proceed without unnecessary friction.

Onboarding controls should adjust based on applicant risk. Digital banks such as Revolut and Chime apply tiered verification models that increase checks when indicators are present. In doing so, they reduce exposure to synthetic identities while allowing lower-risk users to move through the process efficiently.

Authentication should not end at login. Providers such as BioCatch and BehavioSec monitor typing patterns, navigation behavior, and session activity to detect deviations even when credentials are valid. By evaluating activity throughout the session, platforms reduce the likelihood that compromised credentials lead to account takeover.

Fintech transaction monitoring systems conduct transaction checks within the authorization step. For example, networks like Visa and Mastercard assess each transaction in milliseconds, looking at patterns such as how fast a user is making payments, whether the location makes sense, and whether the recipient is trustworthy. This immediate evaluation stops fraud before it can happen, rather than trying to fix it afterward. And because decisions are made before funds are released, this remains the most effective point to prevent loss.

Fraud often involves coordination across accounts. Financial institutions use graph analytics to identify shared devices, repeated beneficiary patterns, and circular fund flows that are not visible when transactions are reviewed individually. When these connections are considered alongside onboarding and authentication data, organized fraud becomes easier to detect.

Each control addresses a specific exposure point. However, their effectiveness ultimately depends on how well the system experience is designed across stages. For this reason, detection weakens when onboarding, authentication, and transaction monitoring operate as separate checkpoints.

Ideally, the risk profile established during onboarding should influence how login activity is evaluated. Authentication outcomes should then shape transaction review. As a result, a payment that appears routine may require closer examination when preceded by a device change or password reset.

When information from each stage informs the next approval decision, earlier signals provide context for later activity, reducing blind spots and improving consistency.

In practice, this requires systems that share information rather than operate independently.

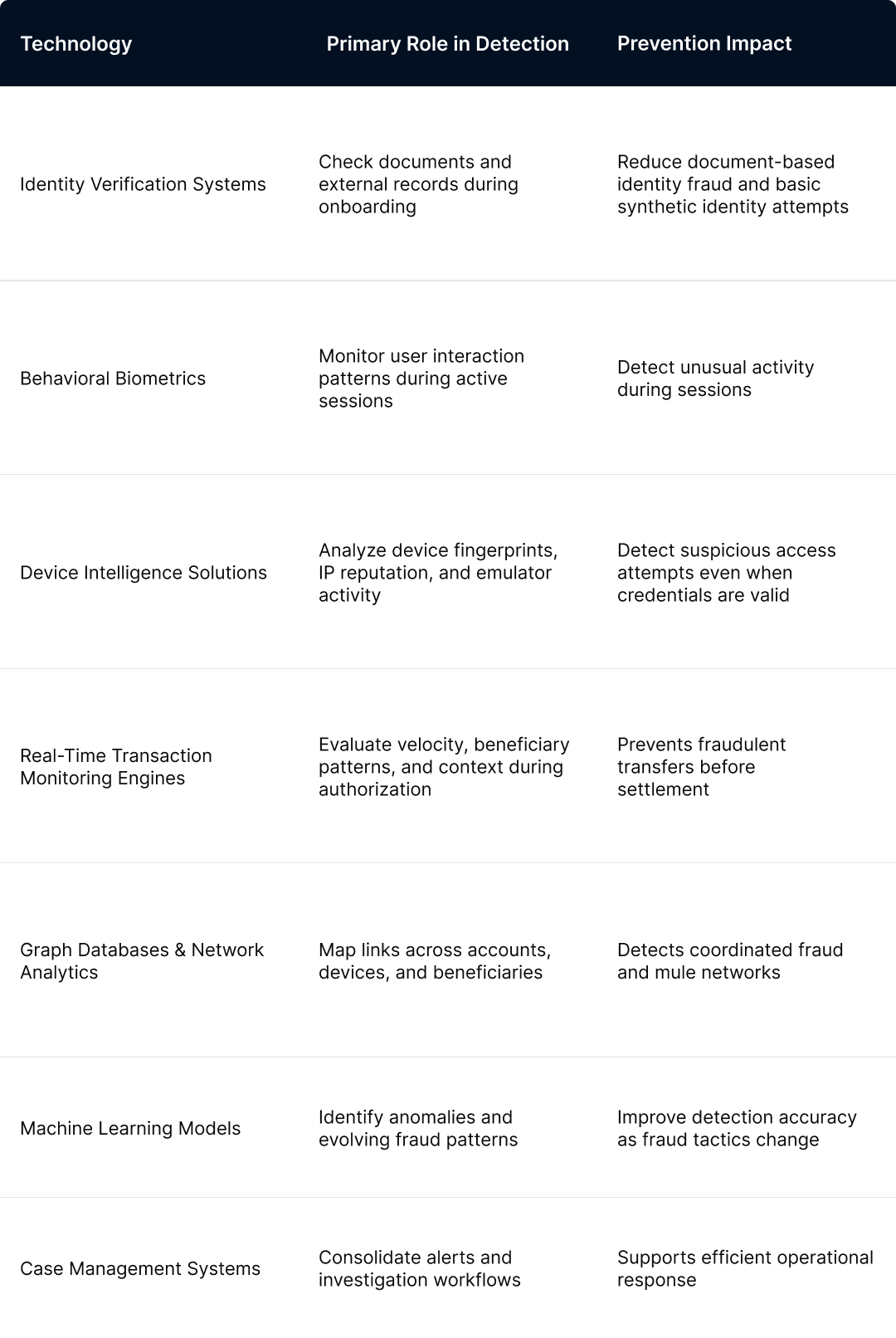

Identity verification tools establish baseline legitimacy during onboarding. Behavioral biometrics and device intelligence monitor activity during active sessions. Monitoring engines evaluate transactions before settlement, while graph analytics identify relationships across accounts, devices, and beneficiaries.

At the same time, financial fraud detection systems use machine learning models to refine detection as patterns evolve, and case management systems support investigation and response.

When these systems share data, decisions become more consistent. Otherwise, gaps reappear.

As fintech systems continue to scale, fraud detection is shifting increasingly toward systems that continuously evaluate risk across the customer lifecycle.

One development driving this shift is the growing use of machine learning to analyze large volumes of transaction and behavioral data. These models can detect patterns that rule-based systems may overlook, allowing detection to adapt as fraud tactics evolve.

Financial institutions are also expanding the use of behavioral profiling. Companies are learning how their customers normally behave, how they log in, what transactions they make, and when. If behavior suddenly looks unusual, the system can step in and ask for extra verification.

Another important focus is spotting coordinated fraud networks. Groups of accounts, devices, or transactions that look normal on their own but reveal a bigger scheme when analyzed together.

As these capabilities develop, fraud detection will increasingly depend on systems that combine behavioral signals, transaction monitoring, and network analysis into a unified decision process.

Ultimately, as fintech systems grow more complex, adding financial fraud detection systems after a product is built leaves gaps that criminals can exploit. What often surprises business leaders is that the fastest-growing platforms are also the most targeted by AI-driven fraud. Attacks using AI, synthetic identities, and coordinated fraud networks move with such speed and sophistication that siloed detection can’t keep up, meaning a platform can appear secure on paper while losing millions in ways traditional reports never reveal.

The smarter approach is to design fraud detection into every step—from onboarding to authentication to transaction approval so that information from one stage shapes the next.

By unifying behavioral patterns, transaction data, and network relationships, leaders can anticipate attacks before they happen, protect customers, and turn fintech fraud detection into a strategic advantage while building platforms that are not only safer but smarter, faster, and more resilient than competitors.